SMM June 26 News:

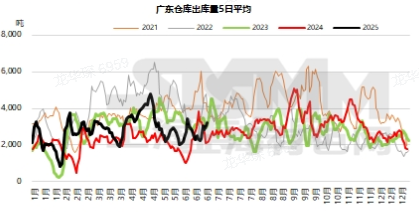

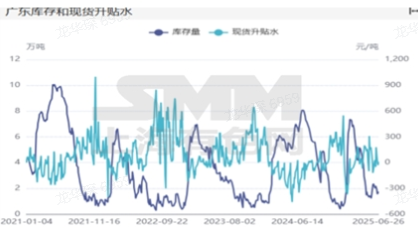

Guangdong region: This week, the premiums and discounts in this region showed a trend of bottoming out and rebounding. At the beginning of the week, influenced by some suppliers' eagerness to liquidate assets by mid-year, premiums continued to decline. However, from Thursday onwards, the situation changed, and premiums began to stop falling and rebound. As of Thursday, high-quality copper was quoted at a premium of 100 yuan/mt, down 80 yuan/mt from last Thursday. Standard-quality copper was quoted at a premium of 10 yuan/mt, down 80 yuan/mt from last Thursday. SX-EW copper was quoted at a discount of 40 yuan/mt, down 80 yuan/mt from last Thursday. On Thursday, the price spread of premiums and discounts for standard-quality copper between Shanghai and Guangdong was 20 yuan/mt higher in Shanghai, with a relatively small spread, leaving no room for cross-regional cargo transfers. According to SMM statistics, as of Thursday, the total inventory in Guangdong warehouses was 17,500 mt, down 1,700 mt from last Thursday. The combined warrants were 4,100 mt, down 4,500 mt from last Thursday. As premiums rebounded, warrants flowed out of the market. Specifically: This week, warehouse arrivals were 14,300 mt/week, up 0.43 mt/week from last week, and on par with the annual average (14,000 mt/week). Domestic copper arrivals increased significantly this week (due to smelters' mid-year inventory clearance), but imported copper arrivals were limited. Outflows from warehouses were 16,100 mt/week, up 4,900 mt/week from last week, and higher than the annual average (14,200 mt/week). It is reported that some warehouses exported copper to the bonded area this week, which was the reason for the significant increase in outflows. Physical consumption was not good this week.

Looking ahead to next week, it is expected that arrivals will not be large due to the continued export of smelters. In terms of downstream consumption, it is reported that some downstream enterprises currently have high finished product inventories and will take production cuts next week. Therefore, we believe that next week will see a decline in both supply and demand, and weekly inventory is expected to continue to decline, but the decline will be limited.

》Subscribe to view SMM metal spot historical prices